The Problem of Deteriorating Financial Soundness in Public Institutions and the Challenges Ahead

-

Writer

CFE

-

Legislative Policy Issue Report No. 5

Legislative Policy Issue Report No. 5

Issues and Liberty

2023.02.07.

1. The Recent Rapid Increase in Public-Sector Debt and the Bill on Managing Insolvent Public Institutions

As of 2021, public-sector debt (D3)—combining the debt of the general government (central and local) and non-financial public enterprises—reached approximately KRW 1,430 trillion, approaching 70% of GDP. This was partly due to the active use of fiscal policy in response to the COVID-19 pandemic, but also largely due to the sharp increase in the debt of public enterprises such as KEPCO and LH. Over the past five years, public-sector debt rose by about KRW 380 trillion (36.4%p), from KRW 1,045 trillion in 2017 to KRW 1,427 trillion in 2021, while the debt of all public institutions increased by about KRW 90 trillion (18.3%p), from KRW 493 trillion in 2017 to KRW 583 trillion in 2021. Public-sector debt appears to have increased sharply primarily under the Moon Jae-in administration.

Some institutions have even begun issuing additional corporate bonds to offset debt or losses, and as the deterioration in the financial soundness of public institutions has recently intensified, the need for concentrated debt management of public institutions has been raised. Accordingly, in July 2022, a partial amendment to the Act on the Management of Public Institutions was submitted by Rep. Eonseok Song as the lead sponsor with 10 co-sponsors (Bill No. 16374). Its main provisions include: 1) requiring the Minister of Economy and Finance to establish financial soundness standards for public institutions; and 2) obligating institutions at financial risk to submit financial soundness plans and reports on financial structure improvement results, including sales revenue, debt ratio, and debt repayment plans.

2. The Continued Deterioration in the Financial Soundness of Public Institutions

◩ The Worsening Financial Soundness of Public Institutions: Financial Risks Centered on Energy/SOC Institutions

To assess the financial soundness of public institutions, one should examine capital, debt, and net income for the period. Total capital of all public institutions increased by about KRW 72 trillion, from KRW 313.7 trillion in 2017 to KRW 386 trillion in 2021. By contrast, debt rose by about KRW 90 trillion, from KRW 493.2 trillion in 2017 to KRW 583 trillion in 2021, meaning debt increased by KRW 18 trillion more than capital. Public institutions are broadly divided into public enterprises, quasi-governmental institutions, and other public institutions. Among them, the debt of public enterprises rose by about KRW 70 trillion, from KRW 364.4 trillion in 2017 to KRW 434.1 trillion in 2021, showing that most of the increase in public-institution debt came from large public enterprises. Net income for the period has also continued to decline over the past five years, recording –KRW 1.8 trillion in 2021. Among institutions with the largest net losses, Korea Electric Power Corporation ranked first with –KRW 5.2 trillion in 2021, the most severe, followed by Korea Railroad Corporation (–KRW 1.2 trillion), Incheon International Airport Corporation (–KRW 750.6 billion), and Korea Racing Authority (–KRW 348.0 billion). In KEPCO’s case, a large net loss occurred due to increased costs caused by a sharp rise in generation fuel prices, including oil prices.

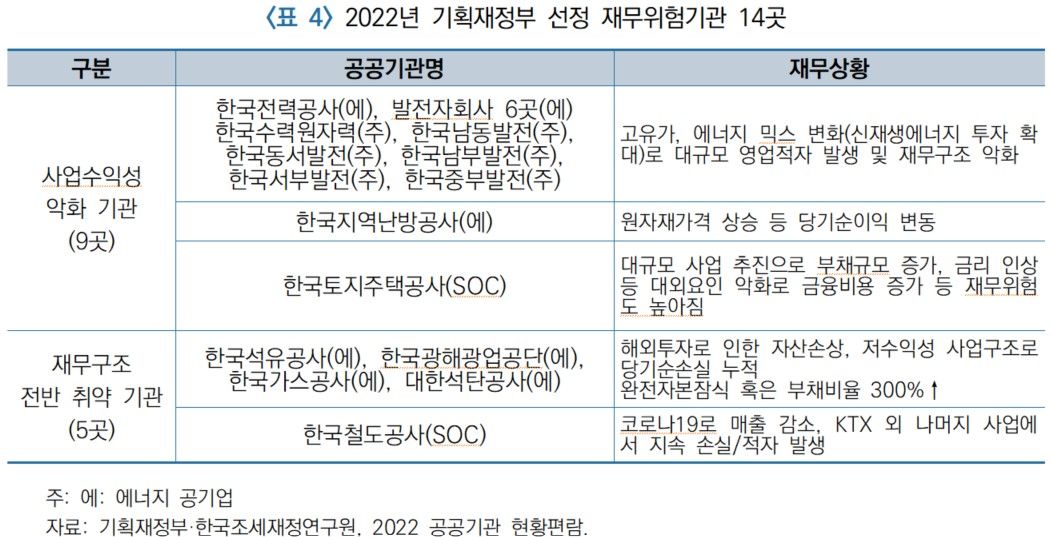

In 2022, the Ministry of Economy and Finance designated 14 institutions as financially at risk. The five most serious were energy public enterprises—Korea National Oil Corporation, Korea Mine Rehabilitation and Mineral Resources Corporation, Korea Gas Corporation, Korea Coal Corporation—and the SOC public enterprise Korea Railroad Corporation.

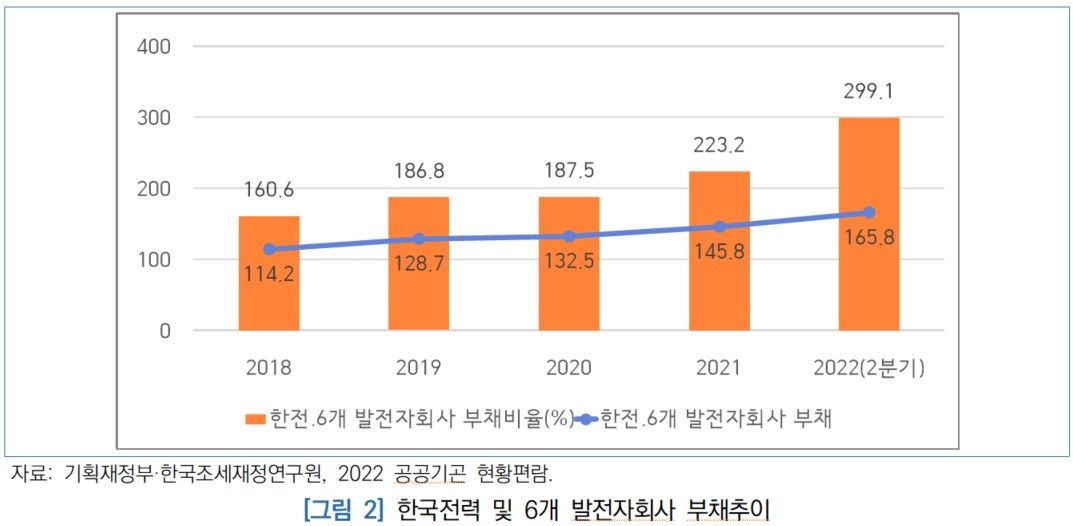

◩ The Worsening Debt of KEPCO and Its Six Power Generation Subsidiaries: KRW 50 Trillion Over the Past Five Years (78% of the Increase in Public Enterprise Debt)

One of the biggest contributors to the increase in public-enterprise debt is the energy sector, namely KEPCO and power generation companies. They were among the 14 public institutions designated by the Ministry of Economy and Finance in June 2022 as financially at risk. The debt of KEPCO and its six power generation subsidiaries increased by about 1.5 times, from KRW 114.2 trillion in 2018 to KRW 165.8 trillion in 2022 (Q2). Their debt ratio rose by about 1.9 times, from 160.6% in 2018 to about 300% in 2022 (Q2). Once the debt ratio exceeds 300%, an institution is classified as being in capital impairment or financial distress; they have reached that level. These conditions stem from 1) persistently high oil prices triggered by the war in Ukraine, and 2) increased borrowing due to the construction of new and replacement power plants and expanded investment in renewable energy as a result of changes in the energy mix, which in turn sharply increased fuel and purchased electricity costs and produced large-scale operating losses.

3. Analysis of the Main Causes and Problems Behind the Deterioration in the Financial Soundness of Public Institutions

◩ Increased Bond Issuance Backed by Government Guarantees, Regardless of Financial Soundness

This was also true in KEPCO’s case, which was the biggest cause of increased public-institution debt: when funds were insufficient for large-scale facility investment, issuing bonds and borrowing externally were the main causes of increased debt (61.5% of total liabilities as of 2019). Public enterprises generally raise external funds not through indirect financing such as bank screening, but mainly through direct financing via bond issuance, and can secure large-scale funding based on their credit ratings without restrictions such as separate collateral or loan covenants (Park Seongyong, 2021). Public institutions can issue bonds at low interest rates through government guarantees regardless of their financial soundness, making this a core cause of worsening financial conditions (Park Seongyong, 2021).

◩ Excessive Regulation of Public Utility Rates Causes Operating Losses and Deficits: Suppressing Rate Increases Is Also a Typical Form of Populism

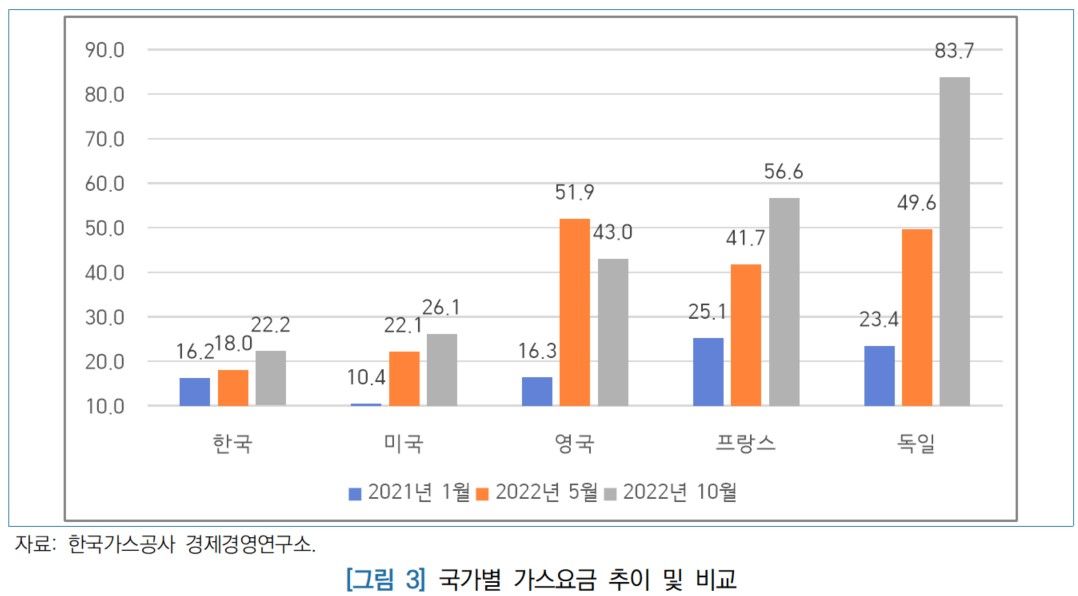

Another major factor increasing the debt of public institutions is a pricing policy that suppresses increases in electricity and gas rates despite rising costs (Choi Junuk, 2014). Recently, the debt of KEPCO, Korea Gas Corporation, and Korea National Oil Corporation has surged due to soaring oil prices, which occurred because public utility rates did not cover costs. For Korea Railroad Corporation, the average cost recovery rate from 2005 to 2018 was only 76.7%, and fares below fully allocated costs resulted in losses totaling KRW 13.7 trillion (Park Seongyong, 2021). Recently, the sharp increase in heating costs (gas rates) has become controversial, but this is because the Moon Jae-in administration failed to properly reflect the continued rise in international gas prices—since all gas is imported—in domestic rates. Compared internationally, Korea’s gas rates are among the lowest in the world, and rates have not been raised appropriately in line with rising global gas prices. Cheap gas prices encourage overconsumption relative to demand, and gas rates below fully allocated cost create a vicious cycle of operating losses and deficits. Excessively suppressing rate increases is also a typical form of populism.

◩ Cost Increases Due to Loose Management: Reckless Investment and Subsidiary Establishment Without Reviewing Business Feasibility

The establishment of subsidiaries through public-institution investment and reckless investment without sufficient feasibility review are also cited as causes of increased debt (Choi Junuk, 2014; National Assembly Budget Office, 2016). The average debt ratio of 36 public-enterprise subsidiaries (Public Institution ALIO) is 232.2%, indicating seriously poor financial soundness. Among the subsidiaries of Korea Midland Power established in December 2018, KOMIPO Service has a debt ratio of 6682.5% and is in a state of capital impairment. It is followed by First Keepers, a subsidiary of Korea Hydro & Nuclear Power (1253%), KEPCO FMS, a subsidiary of KEPCO (966.7%), and Incheon Airport Operation Services, a subsidiary of Incheon International Airport Corporation (785.5%). Most of these institutions are subsidiaries established under the Moon Jae-in administration to convert non-regular workers at public institutions into regular employees, and they have become major factors in the deterioration of financial soundness.

4. Immediate Tasks: Swift Passage of the Bill on Managing Insolvent Public Institutions and Establishment of Financial Soundness Standards by the Ministry of Economy and Finance

To respond to the sharp increase in public-institution debt and the worsening financial soundness led by KEPCO, the bill on managing insolvent public institutions (the amendment to the Act on the Management of Public Institutions), proposed by Rep. Eonseok Song and currently pending before the National Assembly Strategy and Finance Committee, needs to be passed swiftly. The top livelihood-related bill should not be the anti-market amendment to the Grain Management Act, which only causes indiscriminate fiscal waste, but legislation to improve the financial soundness of public institutions. The Ministry of Economy and Finance should promptly establish and enforce strict financial soundness standards for public institutions, including the size of debt and long-term lease liabilities and repayment ratios.

Going forward, based on the principle of full-cost pricing in determining public utility rates, rate increases should be appropriately implemented at a level that compensates for fully allocated costs, even taking the price level into account. In addition, subsidiaries indiscriminately established under the Moon Jae-in administration to convert non-regular workers into regular employees and that have since fallen into capital impairment should be fundamentally reexamined, with privatization or an expansion of private capital participation considered. Choi Junuk (2014), through an international comparison of public-institution debt, found that the higher the degree of privatization, the lower the debt of public enterprises.

◩ References

∙ Partial Amendment Bill to the Act on the Management of Public Institutions, introduced by Rep. Eonseok Song (10 co-sponsors), Bill No. 16374. 2022.7.8.

∙ Ministry of Economy and Finance (2022), Key Contents of the “2022–2026 Mid- to Long-Term Financial Management Plan for Public Institutions.”

∙ Ministry of Economy and Finance · Korea Institute of Public Finance (2022), 2022 Handbook on the Status of Public Institutions.

∙ Park Seongyong (2021), Debt Status of Public Institutions and Measures to Improve Financial Soundness, National Assembly Research Service, Issues and Points No. 1813.

∙ Choi Junuk (2014), Public Institution Debt: Trends, International Comparison, and Discussion of Policy Directions, Korea Institute of Public Finance, Fiscal Forum Current Issue Analysis 1.

∙ Heo Gyeongseon (2013), An Analysis of the Nature and Causes of Public Institution Debt, Korea Institute of Public Finance, Research on Public Institutions 13-02.

Wiki:

https://www.cfe.org/w/bbsDetail.php?&idx=5

Original title: 공공기관 재무건전성 악화의 문제와 당면 과제

Author: Center for Free Enterprise (CFE)

Date: 2023-02-07

Source: https://www.cfe.org/bbs/bbsDetail.php?cid=issue&pn=2&idx=25333